Mid May, many growers were hoping for an end of season with prices around 30 €/100 kg, but rain brought a stop to their hopes… For the last 4 weeks it has been a “weather market” which could still have an influence on prices of the old potato crop.

Processors stopped buying old crop a few weeks ago, some of them even selling contracts they did not need to other processors. Small leftover over tonne volumes were sold with last contract deliveries.

The new crop is starting to arrive on the market whereas all the old crop has not yet been commercialised.

Beginning of season for new crop

New crop, be it earlies (mainly in Germany and Belgium) or maincrop are growing fast and usually developing well. Earlies are between 1 to 2 weeks earlier than usual (with tuber counts which are regularly lower than usual), and in some second earlies first signs of senescence (certainly where less rain fell and higher temperatures recorded) are seen.

Some maincrop fields flowered earlier than usual, without closing the rows, which means that potential production could be on the lower side. Irrigation efficiency (in DE, FR and NL where it is widely used) is not as good as usual, and some irrigation is not done or postponed to higher energy prices.

Weather vagaries (hot spell, heavy rainfall, drought…) past, present and future could bring us some more surprises in the days or weeks to come, through their influence on final yield and quality…

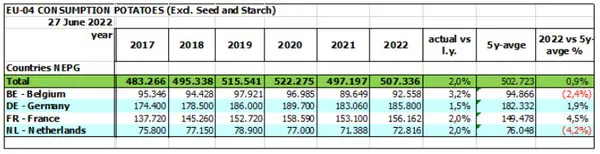

First estimation of potato area in EU-04

The total potato area (first estimation in some cases!) within the NEPG zone (EU-04) has gone up in all 4 countries by 2,0% totalling 507.300 ha, i.e. a plus of 10.100 ha. Compared to the 5 year average, the increase is a 0,9% rise. In late winter early spring, first estimations were that 2022 area would decrease, due to ever higher production costs…

Some starch producers (in DE, FR and NL) and some fresh market potato growers (in DE and FR), are switching their productions to more chipping and crisping potatoes.

CAP 2023 reform and higher production costs are already weighing on possible area 2023

What will the CAP reform bring about for the potato area and production in 2023? High prices for wheat, rape, grain maize… and higher land renting prices could have an influence on future potato hectareage. New environmental constraints related to the European commission proposal to half the use of plant protection products by 2035 could also limit future potato area and/or discourage growers.

Future contract prices should be related to production costs!

In the view of general production costs rises, growers believe that contract prices for the 2023 crop should be related to these increases.

Potato production costs – which have constantly risen during the past 12 months - will definitely have an influence on potato area and production in 2023.

For more information:

Daniel Ryckmans

NEPG

dr@fiwap.be