In the past year or so, a regular influx of smaller vessels on the Transpacific has been seen. In issue 559 of the Sunday Spotlight, we wanted to see if this was indicative of a systemic change or whether it was simply a case of “get in while its good”. To do this, we looked at the 25% quartile vessel size on the Transpacific and Asia-Europe trade lanes.

On Asia-North America West Coast (NAWC), we saw a considerable decrease from a pre-Covid baseline of 6,000-6,500 TEU to just under 4,500 TEU in 2022. Same was the case on Asia-North America East Coast (NAEC), with the figure dropping from a 2020 baseline of 7,500-8,000 TEU to just over 6,000 TEU in 2022. However, to see if this decrease was a result of an influx of smaller vessels relative to the number of services and not simply a case of there being more services in 2022 than there were in 2019, we calculated percentages.

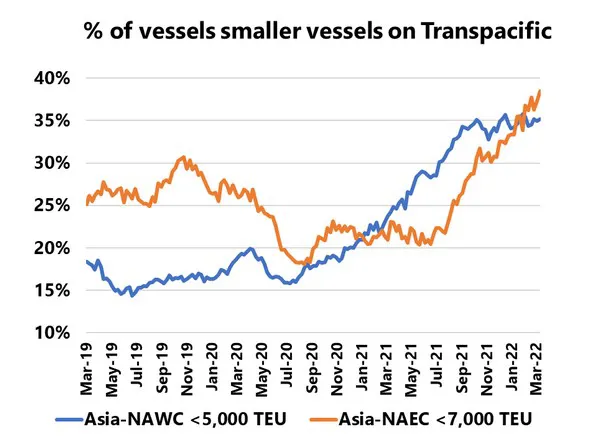

To do this, we calculated percentages. For Asia-NAWC, we calculated the percentage of weekly departures that were under 5,000 TEU, whereas for Asia-NAEC, that figure was for vessels under 7,000 TEU. This classification was based on the average between the pre-pandemic baseline and the current status of the 25% quartile. This is shown in the figure above. On Asia-NAWC, nearly 35% of all weekly departures are under 5,000 TEU, a staggering increase from a pre-pandemic baseline of 15%-20%. On Asia-NAEC, this figure is at nearly 40%, a substantial increase from the 20%-25% level in the first half of 2021.

On Asia-Europe however, there is nothing even close to it as the 25% quartile vessel-size on Asia-North Europe is within normal seasonality, while on Asia-Mediterranean, the 25% quartile vessel-size is largely unchanged from 2019. We know that niche carriers did launch services on Asia-Europe, but they were seasonal in nature and hardly had an impact, whereas on the Transpacific, we see a systemic influx of smaller vessels. This also shows that even though both trades are often viewed through the same lens, there are fundamental differences between the two, especially in todays pandemic-impacted market.

For more information: sea-intelligence.com